Business

Silicon Valley Lawmaker Explores Legislation After Bank Collapse

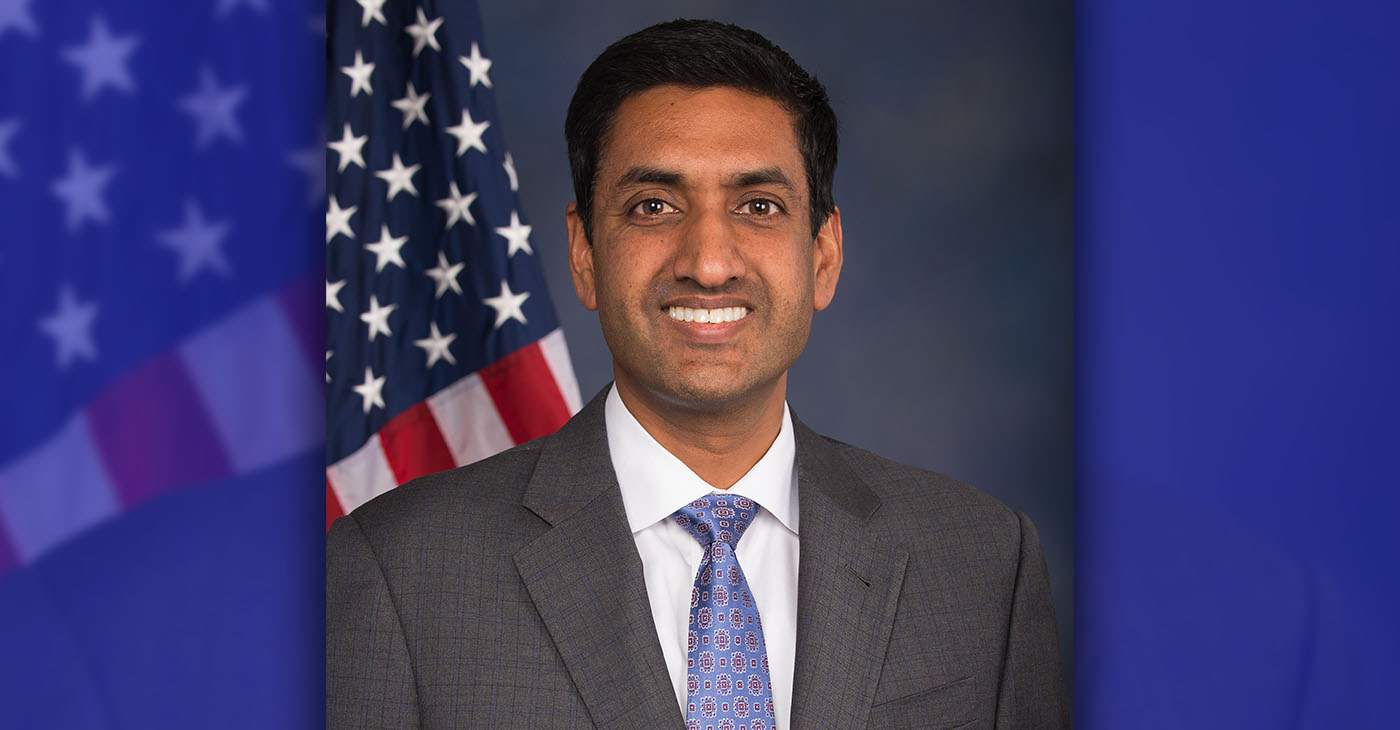

Two weeks after Silicon Valley Bank’s collapse left thousands of businesses reeling, one Silicon Valley lawmaker is exploring legislation to ensure it doesn’t happen again. At a discussion in Santa Clara on Saturday with nonprofit and business leaders, Congressman Ro Khanna announced he’s crafting legislation that would require banks to pay higher premiums to the Federal Deposit Insurance Corporation (FDIC) to protect all account holders — including those with funds higher than $250,000. The revenue would protect deposits in case of a collapse.

By Jana Kadah

San Jose Spotlight

Two weeks after Silicon Valley Bank’s collapse left thousands of businesses reeling, one Silicon Valley lawmaker is exploring legislation to ensure it doesn’t happen again.

At a discussion in Santa Clara on Saturday with nonprofit and business leaders, Congressman Ro Khanna announced he’s crafting legislation that would require banks to pay higher premiums to the Federal Deposit Insurance Corporation (FDIC) to protect all account holders — including those with funds higher than $250,000. The revenue would protect deposits in case of a collapse.

“I think (this legislation) is promising if I can get a Republican to sign on,” Khanna told San Jose Spotlight. “Right now, you basically have large accounts acting as uninsured drivers. The government ends up covering them if they fail, but they’re not paying for the insurance beyond $250,000, so we need to have some fees and some insurance.”

Financial regulators abruptly closed Silicon Valley Bank on March 10 after uncertainty about its solvency led to a massive bank run. The bank’s failure is the second largest in U.S. history and SVB reportedly held $209 billion in assets at the time of its collapse.

The closure sent a wave of panic among thousands of tech businesses, nonprofits and startups that questioned how they’d make payroll and keep their doors open without access to their funds.

The Federal Reserve Board said all depositors at Silicon Valley Bank could access their money the following Monday — three days after the collapse — including funds beyond the $250,000 insurance cap. The announcement led to lines wrapping around the bank’s headquarters in Santa Clara with anxious account holders waiting to pull their money.

Still, two weeks later, many business leaders are apprehensive about the future.

Marie Bernard, CEO of homeless prevention nonprofit Sunnyvale Community Services, said she’s worried about a SVB loan taken out to pay for her nonprofit’s new office. If the loan falters, the nonprofit will be forced to foot the bill and cut back services like rent relief and food for needy residents. She’s relieved the nonprofit’s $1 million in the bank is safe.

“We still don’t know what’s going on with the loan (for the new office space),” Bernard said at the Saturday discussion. “We’re on pins and needles until we can either raise the remaining money for the mortgage, or we find that we can potentially refinance.”

Austin Sendek, co-founder and CEO of climate-tech startup Aionics, Inc, which uses artificial intelligence to find environmental solutions, said climate-tech businesses like his struggle to get investments.

“Climate tech is already seen as a somewhat risky investment, so when you get those investment dollars in your bank account, you want to protect them,” Sendek said. “We’re (also) going into a macro-economic environment where venture capital seems to be sort of becoming a little bit harder to come by.”

Without protection from the FDIC, Sendek said a generation of climate-tech startups in the region would be wiped out financially and struggle to secure future investments.

Nico Pinkowski, CEO of Nitricity Inc — a startup that transforms water, air and solar into nitrogen fertilizer — said now that he’s made payroll and vendor payments, his biggest worry is how SVB’s failure may impact other regional banks. Deposits at small U.S. banks dropped dramatically in the week following the collapse of Silicon Valley Bank on March 10, data by the Federal Reserve showed.

He said climate-tech companies like his survive because of the flexibility regional banks can provide.

“We need these banks to continue to be there and we need to rebuild trust,” Pinkowski said. “Any and all ways the government can support rebuilding of trust makes ultimately a very large difference for companies like ours.”

Khanna said Americans should feel confident in the U.S. banking industry. In the last 10 years, 73 banks have failed and the depositors at all of them were made whole, he said. In response to criticism that the government is bailing out billionaires, Khanna said SVB’s situation is different from the 2008 financial crisis because the protection is for small businesses, nonprofits and tech startups — not bank executives and shareholders.

“(This wasn’t) just bailing out the rich people in Silicon Valley,” Khanna said. “These were the climate tech startups. These were the startups at biotech. And these were a lot of organizations that were actually serving the community.”

Activism

Oakland Post: Week of February 25 – March 3, 2026

The printed Weekly Edition of the Oakland Post: Week of – February 25 – March 3, 2026

To enlarge your view of this issue, use the slider, magnifying glass icon or full page icon in the lower right corner of the browser window.

Activism

Chase Oakland Community Center Hosts Alley-Oop Accelerator Building Community and Opportunity for Bay Area Entrepreneurs

Over the past three years, the Alley-Oop Accelerator has helped more than 20 Bay Area businesses grow, connect, and gain meaningful exposure. The program combines hands-on training, mentorship, and community-building to help participants navigate the legal, financial, and marketing challenges of small business ownership.

By Carla Thomas

The Golden State Warriors and Chase bank hosted the third annual Alley-Oop Accelerator this month, an empowering eight-week program designed to help Bay Area entrepreneurs bring their visions for business to life.

The initiative kicked off on Feb. 12 at Chase’s Oakland Community Center on Broadway Street, welcoming 15 small business owners who joined a growing network of local innovators working to strengthen the region’s entrepreneurial ecosystem.

Over the past three years, the Alley-Oop Accelerator has helped more than 20 Bay Area businesses grow, connect, and gain meaningful exposure. The program combines hands-on training, mentorship, and community-building to help participants navigate the legal, financial, and marketing challenges of small business ownership.

At its core, the accelerator is designed to create an ecosystem of collaboration, where local entrepreneurs can learn from one another while accessing the resources of a global financial institution.

“This is our third year in a row working with the Golden State Warriors on the Alley-Oop Accelerator,” said Jaime Garcia, executive director of Chase’s Coaching for Impact team for the West Division. “We’ve already had 20-plus businesses graduate from the program, and we have 15 enrolled this year. The biggest thing about the program is really the community that’s built amongst the business owners — plus the exposure they’re able to get through Chase and the Golden State Warriors.”

According to Garcia, several graduates have gone on to receive vendor contracts with the Warriors and have gained broader recognition through collaborations with JPMorgan Chase.

“A lot of what Chase is trying to do,” Garcia added, “is bring businesses together because what they’ve asked for is an ecosystem, a network where they can connect, grow, and thrive organically.”

This year’s Alley-Oop Accelerator reflects that vision through its comprehensive curriculum and emphasis on practical learning. Participants explore the full spectrum of business essentials including financial management, marketing strategy, and legal compliance, while also preparing for real-world experiences such as pop-up market events.

Each entrepreneur benefits from one-on-one mentoring sessions through Chase’s Coaching for Impact program, which provides complimentary, personalized business consulting.

Garcia described the impact this hands-on approach has had on local small business owners. He recalled one candlemaker, who, after participating in the program, was invited to provide candles as gifts at Chase events.

“We were able to help give that business exposure,” he explained. “But then our team also worked with them on how to access capital to buy inventory and manage operations once those orders started coming in. It’s about preparation. When a hiccup happens, are you ready to handle it?”

The Coaching for Impact initiative, which launched in 2020 in just four cities, has since expanded to 46 nationwide.

“Every business is different,” Garcia said. “That’s why personal coaching matters so much. It’s life-changing.”

Participants in the 2026 program will each receive a $2,500 stipend, funding that Garcia said can make an outsized difference. “It’s amazing what some people can do with just $2,500,” he noted. “It sounds small, but it goes a long way when you have a plan for how to use it.”

For Chase and the Warriors, the Alley-Oop Accelerator represents more than an educational initiative, it’s a pathway to empowerment and economic inclusion. The program continues to foster lasting relationships among the entrepreneurs who, as Garcia put it, “build each other up” through shared growth and opportunity.

“Starting a business is never easy, but with the right support, it becomes possible, and even exhilarating,” said Oscar Lopez, the senior business consultant for Chase in Oakland.

Activism

Oakland Post: Week of February 18 – 24, 2026

The printed Weekly Edition of the Oakland Post: Week of – February 18 – 24, 2026

To enlarge your view of this issue, use the slider, magnifying glass icon or full page icon in the lower right corner of the browser window.

WORK FROM HOME

Home-based business with potential monthly income of $10K+ per month. A proven training system and website provided to maximize business effectiveness. Perfect job to earn side and primary income. Contact Lynne for more details: Lynne4npusa@gmail.com 800-334-0540

![]()

Poll Shows Support for Policies That Help Families Afford Child Care

Oakland Post: Week of February 25 – March 3, 2026

Trump’s MAGA Allies are Creating Executive Order Plan to Steal the 2026 Midterms

PRESS ROOM: NBA Hall of Fame Nominee Terry Cummings Joins 100 Black Men of DeKalb County to Launch Victory & Values Initiative

Reflecting on Black History Milestones in Birmingham AL

OP-ED: One Hundred Years of Black Workers Telling the Truth

PRESS ROOM: Civil Rights TV Launches in Selma as the World’s First 24/7 Civil Rights Television Network

Advancements in solar technology that are changing the way we power the world

U.S. manufacturing rebounds – how foundry services are adapting to rising demand

Why has blood testing become so popular in today’s world?

Ghana Mourns a Son of the African World

OP-ED: Trump’s Policies Hurt Black America—and Everyone Else

OP-ED: Meta Deleted Me. I Still Don’t Know Why. And neither will you.

More than a Mission: Paying It Forward for the Future of Education

Avoid Eviction This Season: Landlord Checklist for Stable Tenancies

Oakland Post: Week of January 28, 2025 – February 3, 2026

Life Expectancy in Marin City, a Black Community, Is 15-17 Years Less than the Rest of Marin County

Community Celebrates Turner Group Construction Company as Collins Drive Becomes Turner Group Drive

California Launches Study on Mileage Tax to Potentially Replace Gas Tax as Republicans Push Back

Discrimination in City Contracts

Book Review: Books on Black History and Black Life for Kids

Oakland Post: Week of January 21 – 27, 2026

COMMENTARY: The Biases We Don’t See — Preventing AI-Driven Inequality in Health Care

Post Newspaper Invites NNPA to Join Nationwide Probate Reform Initiative

Medi-Cal Cares for You and Your Baby Every Step of the Way

Black History Events in the East Bay

Art of the African Diaspora Celebrates Legacy and Community at Richmond Art Center

COMMENTARY: The National Protest Must Be Accompanied with Our Votes

New Bill, the RIDER Safety Act, Would Support Transit Ambassadors and Safety on Public Transit

After Don Lemon’s Arrest, Black Officials Raise Concerns About Independent Black Media

Hyundai Ioniq 5 Parking, Safety, and 360 View #shorts

2025 Ioniq 5 New Wiper & Powerful Performance! #shorts

Electric SUV Range: Is 259 Miles Enough? #shorts

EV Charging: How Fast Can You Charge an Electric Vehicle? #shorts

Biometric Cooling… Messaging Seats…Come on! 2025 Infiniti QX80 Autograph 4WD

Charged Up: Witness the Magic of a Fully Electric Car! #shorts

Range Rover Sport PHEV Included…: See What’s Inside This Luxury SUV! #shorts

Invisible Hood View: Perfect Parking with X-Ray Vision! #shorts

AI Is Reshaping Black Healthcare: Promise, Peril, and the Push for Improved Results in California

ESSAY: Technology and Medicine, a Primary Care Point of View

Sanctuary Cities

The RESISTANCE – FREEDOM NOW

STATE OF THE PEOPLE: Freddie

ECONOMIC BOYCOTT DAY!!!!!

I told You So

-

Activism4 weeks ago

Activism4 weeks agoCommunity Celebrates Turner Group Construction Company as Collins Drive Becomes Turner Group Drive

-

Business4 weeks ago

Business4 weeks agoCalifornia Launches Study on Mileage Tax to Potentially Replace Gas Tax as Republicans Push Back

-

Activism4 weeks ago

Activism4 weeks agoDiscrimination in City Contracts

-

Arts and Culture4 weeks ago

Arts and Culture4 weeks agoBook Review: Books on Black History and Black Life for Kids

-

Activism4 weeks ago

Activism4 weeks agoCOMMENTARY: The Biases We Don’t See — Preventing AI-Driven Inequality in Health Care

-

Activism4 weeks ago

Activism4 weeks agoPost Newspaper Invites NNPA to Join Nationwide Probate Reform Initiative

-

Alameda County4 weeks ago

Alameda County4 weeks agoBlack History Events in the East Bay

-

Activism4 weeks ago

Activism4 weeks agoArt of the African Diaspora Celebrates Legacy and Community at Richmond Art Center